| Map

> Data Science > Predicting the Future >

Modeling > Regression

> Multiple Linear Regression |

|

|

|

|

|

|

Multiple Linear

Regression

|

|

|

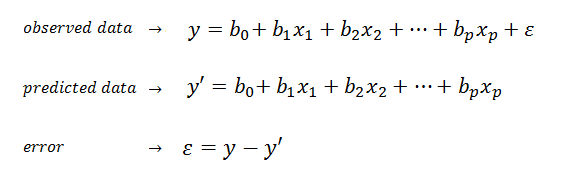

| Multiple linear regression (MLR) is a method used to model the linear relationship between a

dependent variable (target) and one or more independent variables

(predictors). |

|

|

|

|

|

|

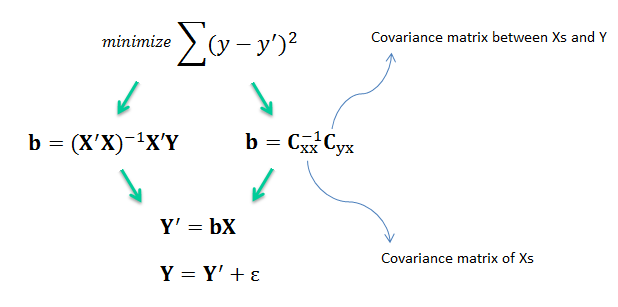

| MLR is based on ordinary least squares (OLS), the model is fit such that the sum-of-squares of differences of observed and predicted

values is minimized. |

|

|

|

|

|

|

| The MLR model is based on several

assumptions (e.g., errors are normally distributed with zero mean and constant variance). Provided the assumptions are satisfied, the regression

estimators are optimal in the sense that they are unbiased, efficient, and

consistent. Unbiased means that the expected value of the estimator

is equal to the true value of the parameter. Efficient means that the estimator has a smaller variance than any

other estimator. Consistent means that the bias and variance of the estimator approach zero as the sample size

approaches infinity. |

|

|

|

|

|

| How good is the model? |

|

|

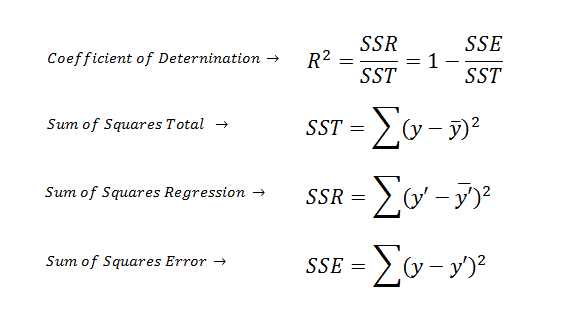

| R2 also called as coefficient

of determination summarizes the explanatory power of the regression

model and is computed from the sums-of-squares terms. |

|

|

|

|

|

|

| R2 describes the proportion of variance

of the dependent variable explained by the regression model. If the regression

model is “perfect”, SSE is zero, and R2 is 1. If the regression

model is a total failure, SSE is equal to SST, no variance is explained by regression, and

R2 is zero. It is important to keep in mind that there is no

direct relationship between high R2 and causation. |

|

|

| |

|

|

| How significant is the model? |

|

|

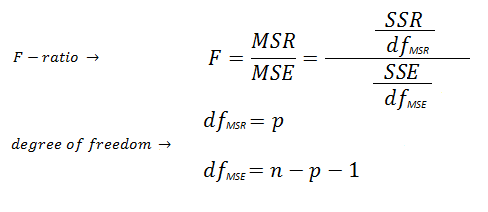

| F-ratio estimates the

statistical significance of the regression model and is computed from the

mean squared terms in the ANOVA table. The significance of the F-ratio is obtained by referring to

the F distribution table using two degrees of freedom (dfMSR,

dfMSE). p

is the number of independent variables (e.g., p

is one for the simple linear regression). |

|

|

|

|

|

|

| The advantage of the F-ratio over R2 is that

the F-ratio incorporates sample size and number of predictors in assessment of significance of the

regression model. A model can have a high R2 and still not be statistically significant. |

|

|

| |

|

|

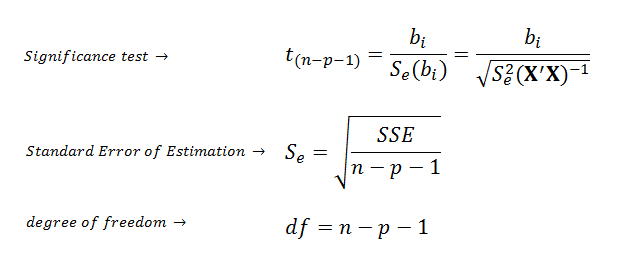

| How significant are the

coefficients? |

|

|

| If the regression model is

significantly good, we can use t-test to estimate the statistical

significance of each coefficient. |

|

|

|

|

|

|

| Example |

|

|

| |

|

|

| Multicolinearity |

|

|

| A high degree of multicolinearity

between predictors produces unreliable regression coefficient estimates. Signs of multicolinearity include: |

|

|

- High correlation between pairs of predictor

variables.

- Regression coefficients whose signs or magnitudes do not make

good physical sense.

- Statistically nonsignificant regression coefficients on important

predictors.

- Extreme sensitivity of sign or magnitude of

regression coefficients to insertion or deletion of a predictor.

|

|

|

| The diagonal values in the (X'X)-1

matrix called Variance Inflation

Factors (VIFs) and they are very useful measures of multicolinearity.

If any VIF exceed 5, multicolinearity is a problem. |

|

|

| |

|

|

| Model Selection |

|

|

| A frequent problem in data mining is to

avoid predictors that do not contribute significantly to model prediction.

First, It has been shown that dropping

predictors that have insignificant coefficients can reduce the average error of predictions.

Second, estimation of regression coefficients are likely to be unstable due to multicollinearity

in models with many variables. Finally, a simpler model is a better model

with more insight into the influence of predictors in models. There

are two main methods of model selection: |

|

|

- Forward selection, the best predictors are

entered in the model, one by one.

- Backward Elimination, the

worst predictors are eliminated from the model, one by one.

|

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

|